You send $200,000 to your German machinery supplier from a bank that charges a $35 wire fee. It seems reasonable enough, until you realize the cost was actually closer to $6,035. That 3% exchange rate markup your bank never itemized? It just quietly removed $6,000 from your transfer. According to Wise research, US small businesses collectively lost nearly $800 million to hidden exchange rate markups in 2023.

Globally, corporations lose $120 billion a year in cross-border transaction fees alone. And despite the rise of fintech alternatives, 76% of SME cross-border payments still flow through traditional banks. If you're a Florida business owner sending payments to Europe, here's what your bank statement isn't showing you.

Walk into any Florida bank and ask about sending money overseas. They'll offer you a flat wire fee: typically $35 to $45. One regional bank in Coral Gables charges around $35 per outgoing international wire, while a well-known Miami-based institution charges $45, and one of the country's largest national banks charges $45 for a USD international wire.

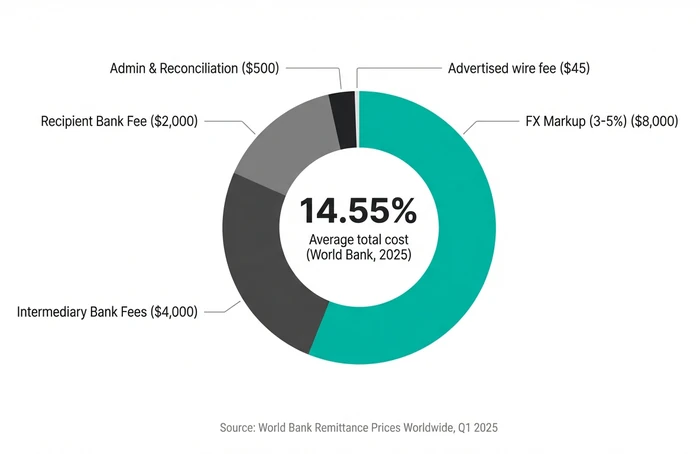

These numbers feel manageable. Predictable. But they're the tip of the iceberg. According to the World Bank's Q1 2025 Remittance Prices report, the average total cost of sending international transfers through traditional banks is 14.55% when all fees — wire fees, intermediary charges, and FX markups — are combined. That's nearly three times what non-bank providers charge.

The real cost of wiring money is buried in the exchange rate. Traditional banks apply a 3% to 5% markup over the mid-market rate, which is the rate you'd see on Google or Reuters. This markup is never disclosed as a separate line item on your wire receipt. It's baked into the rate itself, invisible unless you know exactly where to look.

Here's the thing: even banks that advertise "no wire fees" on foreign currency transfers aren't giving you a free ride. One major national bank, for example, waives the wire fee on FX transactions over $5,000 — but its own fee schedule explicitly states that the "no fee" benefit doesn't cover the exchange rate spread. Another top-tier bank's disclosures similarly note that it "may make money" on the exchange rate. The fee didn't disappear, it just changed shape.

Once you click "send" on a SWIFT wire, your money enters what is essentially a black hole. Here's what actually happens behind the scenes.

Your payment doesn't travel directly from your bank in Miami to your supplier's bank in Frankfurt. Instead, it passes through two to four intermediary, or "correspondent" banks. Each one acts as a relay point in the SWIFT network. And each one can deduct its own processing fee mid-transit, without notifying you or your recipient.

The result is what's known in the industry as "short payments." You wire $200,000, but your German supplier receives $198,600. The missing $1,400 was siphoned off by correspondent banks along the way. Now your supplier is short on their invoice, your accounts payable team has to reconcile the discrepancy, and someone needs to send a supplementary payment to cover the gap. In business owner forums, finance managers describe adding a "5 to 10% buffer" to wire amounts just to ensure that the full invoiced amount actually arrives.

Most business owners focus on the wire fee because that's the number their bank shows them. But the true total cost of ownership for a Florida-to-Europe wire involves five separate cost layers — and only one of them appears on your statement.

*Fees shown are illustrative. Actual costs may vary based on client classification, transaction volume, compliance requirements, and applicable regulatory considerations.

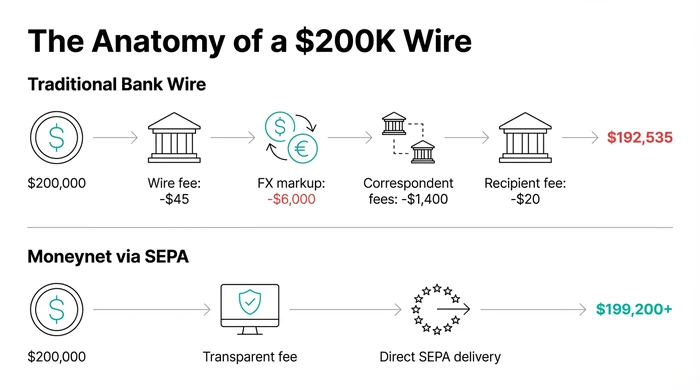

On a single $200,000 transfer, illustrated above, the traditional bank column adds up to $6,100 to $10,100 in total costs. The fintech column? Closer to $600 to $2,000. Multiply that difference across a year of monthly payments, and you're looking at tens of thousands of dollars quietly leaking out of your business.

What's more, the traditional banking model charges you extra in time. The three-to-five-day settlement window means your working capital sits frozen in transit. For businesses managing multiple European supplier relationships simultaneously — common across Florida's $7.15 billion Germany trade corridor and $5.75 billion UK corridor — that's a significant amount of cash flow locked up at any given moment.

Florida businesses don't have to accept hidden fees and opaque processes as the cost of doing business in Europe. Fintech platforms have fundamentally re-engineered how cross-border payments work, and Moneynet is purpose-built for businesses that need clarity and control over their international payments.

With Moneynet, you see the exact cost before you send: the exchange rate, the fee, and the total amount your recipient will receive. There are no hidden FX markups, and no surprise deductions mid-transit. The amount that you quote to your European partner is the amount that arrives in their account.

Instead of routing your payment through the SWIFT correspondent chain, Moneynet delivers EUR payments directly through SEPA, the eurozone's domestic clearing network. This bypasses intermediary banks entirely, which means no mid-transit deductions and no short payments. Your German or French supplier receives the funds as a local transfer, often on the same day or next business day.

No more calling your bank to ask "where's my money?" Moneynet provides live status updates from initiation to credit, with webhook notifications and downloadable payment proofs. You know exactly where your funds are at every stage; and so does your supplier.

Moneynet offers competitive, transparent exchange rates — a fraction of the 3% to 5% markup traditional banks embed in their quotes. You see the exact rate and fee before you confirm, so you know precisely what you're paying. On a $200,000 transfer, that difference can save you thousands of dollars per transaction.

Moneynet is authorized by the UK Financial Conduct Authority (Reference No. 900190) and holds US Money Transmitter licenses, including in Florida. Every transaction passes through automated KYC, AML, and sanctions screening. And advanced encryption and two-factor authentication protect your data and funds at every step.

You won't navigate an automated phone tree. Moneynet provides personal, responsive account management: real people who understand cross-border payments and can help you map the most efficient corridors and rails for your specific European payment needs.

Every dollar lost to a hidden exchange rate markup is a dollar that could fund your next equipment purchase, your next hire, or your next market expansion. Florida's position as a transatlantic trade powerhouse means European payments will remain a mainstay. The hidden costs, on the other hand, are not inevitable.

Ready to see what your European payments actually cost? Talk to Moneynet and get a transparent quote with no hidden markups and no surprises. Book a consultation today and take control of your cross-border payments.